The first infrastructure bank bill was proposed by Congress in 2007, and some iteration of it has been reintroduced in every Congress since. Beginning in 2009, the Obama Administration identified the creation of a National Infrastructure Bank (NIB) as an important goal for enhancing surface transportation financing. The President recently renewed that call in a speech in New Orleans last November.

The decline of the US’s transportation infrastructure is well documented. A number of high profile bridge collapses have occurred in recent years, in particular that of an I-5 bridge in Washington State in May of 2013 and the catastrophic collapse of the I-35W Mississippi River Bridge in 2007 that killed 13 people. Travelers who rely on urban rail systems such as Chicago’s CTA and Washington’s WMATA often face long delays due to a backlog of maintenance projects, and Washington DC’s Red Line into Maryland may be shut down for several weeks in the coming year for urgent repairs.

Efforts to build high-speed rail have been slow going despite their popularity in Western Europe, Japan, China, and elsewhere. The endorsement of the Administration, state programs such as the California High Speed Rail Authority project, and the recognition that a more efficient surface transportation system is a component of the fight against climate change have done little to bolster Congressional support. Furthermore, the GOP takeover of the House of Representatives has completely dried up federal funds for high-speed rail and limited support for conventional rail programs as well.

MAP-21 Authorizations, the Gas Tax, and the Structural Shortfall

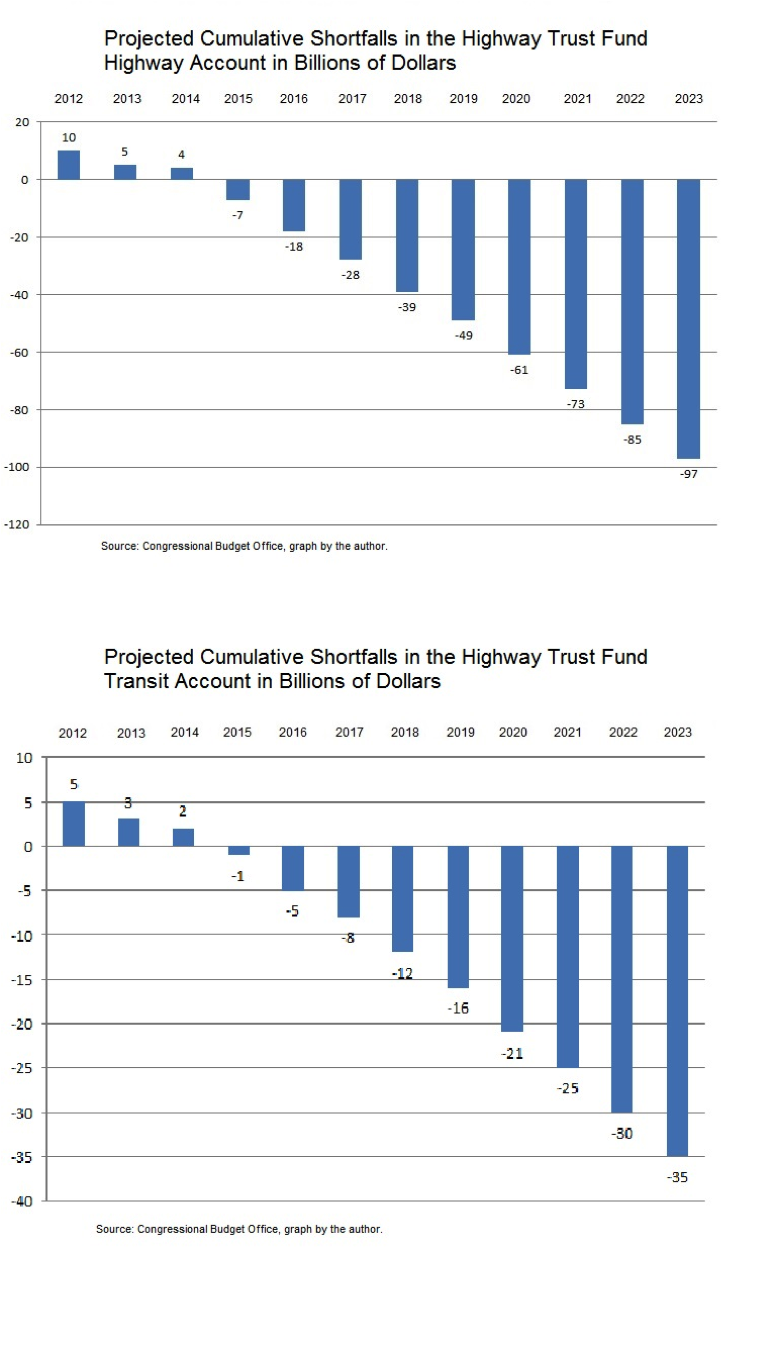

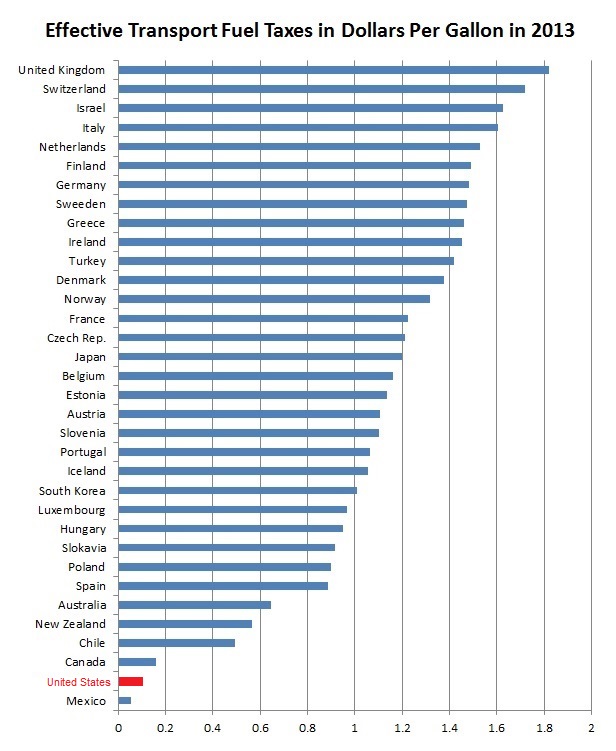

Surface transportation funding at the federal level is currently authorized by the Moving Ahead for Progress in the 21st Century Act (MAP-21). The act provides for approximately $105 billion of federal financing for surface transportation over its two year life (it is set to expire at the end of fiscal year 2014). As the bulk of the funding for MAP-21’s projects comes from the federal gas tax’s Highway Trust Fund, federal transportation spending is in principle largely insulated from the year-to-year appropriations process, and is therefore non-discretionary spending. However, much of that non-discretionary nature has slipped away as rising fuel efficiency has lowered gas tax revenue and driving, especially among millennials, has declined. The gas tax has been fixed at the same level, $0.18 per gallon, since 1993. It is important to realize that the gas tax is not a sales tax or VAT, but a tax on each gallon of gas sold. Thus, as the dollar inflates, and if people use less gas, tax revenues whittle away. The US rate is the lowest among OECD countries, and there seems to be little consensus on raising or replacing it in Congress. The Highway Trust Fund required a bailout of $35 billion in federal appropriations from 2008 to 2010 to keep it solvent, and its long term ability to fund surface transportation needs is doubtful in its current form.

|

Current Federal Highway Taxes Per Gallon |

|||||

|

Distribution of the Tax |

|||||

|

Tax Rate |

Effective Date |

Highways |

Mass Transit |

Other* |

|

|

Gas |

$0.184 per gallon |

Oct. 1, 1997 |

$0.1544 |

$0.0286 |

$0.001 |

|

Gasohol |

$0.184 per gallon |

Jan. 1, 2005 |

$0.1544 |

$0.0286 |

$0.001 |

|

Diesel |

$0.244 per gallon |

Oct. 1, 1997 |

$0.2144 |

$0.0286 |

$0.001 |

* Leaking Underground Storage Tank Trust Fund

This federal funding law was preceded by several other authorizations and highway aid programs. In recent years, increasing shares of the gas tax are being committed to non-automobile projects, such as passenger rail, bicycle paths, and other forms of “alternative” transportation.

In addition to grants, the US Department of Transportation (DOT) administers two relatively small loan programs that have some of the characteristics of the National Infrastructure Bank proposal. The first is the Railroad Rehabilitation and Improvement Financing (RRIF) program, which provides long-term, low interest loans to freight and passenger railroads. The second is the Transportation Infrastructure Finance and Innovation Act (TIFIA) program, which similarly provides credit assistance to surface transportation projects. For high-speed rail and freight railroads, RRIF and TIFIA provide financing that the private market will not. For agencies building rail transit systems (and are not able to cover their operating expenses from fares), these programs can accelerate a project’s financing and construction schedule. Loan are supposed to be paid back by state or local tax revenue, or by conventional transportation grants over the loan’s long life and low interest rates. Experts, including the Brookings Institution’s Robert Puentes, have suggested expanding both programs.

The National Infrastructure Bank and Private Equity

The political difficulties of raising taxes, combined with an increasing emphasis on public-private partnerships, has led many in surface transportation policy circles to examine the idea of an infrastructure bank. An NIB would largely rely on bond financing and would encourage public-private partnerships in the financing and running of public infrastructure. Public-private partnerships are already being increasingly used to fund and contract-out the management of highway and transit projects. Depending on the exact structure enacted, an NIB would probably be a quasi-public entity like the Federal Deposit Insurance Corporation (FDIC) or the Federal Reserve System. Infrastructure banks are a common way to fund infrastructure in, Japan, and other developed countries.

There is currently one NIB bill in the House of Representatives—H.R. 2084 by Rep. Delaney (D-MD). The bill has 50 co-sponsors, half of which are Democrats and half of which are Republicans. A notable feature of the bill is a “repatriation” tax holiday for US corporations sheltering capital overseas.

In the absence of policy advancement at the federal level, local jurisdictions such as Los Angeles have examined leveraging and accelerating their local tax revenues via loans from foreign investment banks. Denver’s transportation authority has entered into a $2.75 billion public-private construction and concessionaire arrangement for one of their rail projects. This is the largest rail transit P3 to date.

An NIB in the US Context

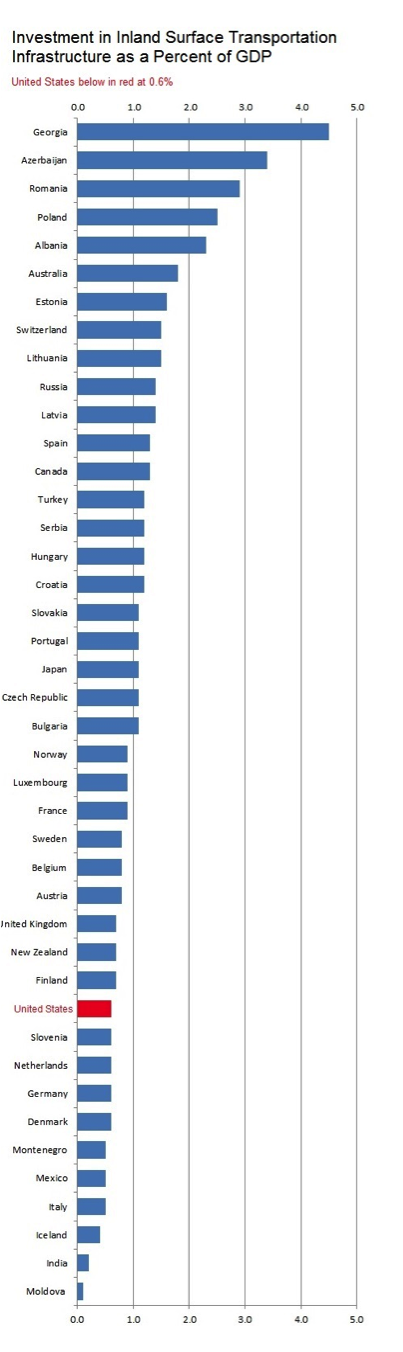

Several countries in the OECD use infrastructure banks. However, none of them have motor fuel taxes funding infrastructure as low as those in the US. Similarly the US is an outlier in surface transportation spending as a percentage of GDP. The data bears this out rather starkly.

Several negative consequences could follow from the mismatch of attempting to graft a large infrastructure bank process onto a deficient public financing system. These include:

- Pushing off raising taxes onto state and local governments. States and local jurisdictions likely have practical political and macroeconomic constraints to their ability to raise revenue that the federal government does not.

- Excessive reliance on P3 concessionaire structures for public infrastructure and finance likely have political limits both locally and nationally. A recent P3 deal for high-speed rail in Taiwan met ridership projections but the private financing was excessively leveraged vis-à-vis the public component, requiring a government buyout of the consortium.

- Financing deals with private equity through the NIB will further strain already limited local and federal public funding sources such as the federal gas tax, further exacerbating the current insolvency of the Highway Trust Fund. These funds as well as state and local sources will be needed to help leverage NIB and other private capital.

So You Thought There Was A Private Sector Only Solution

While a National Infrastructure Bank would be an improvement over the status quo, it would not solve long term public funding shortfalls in infrastructure. In fact, a successful bank would further burden the already strained public financing mechanism. To solve the US’s infrastructure crisis and get the most value out of public-private partnerships like the NIB, federal revenue sources need to be increased and spending brought up to the mean level of the OECD. A phased raising and indexing of the gas tax coupled with a new, more robust surface transportation authorization than the soon-to-expire MAP-21 are the likely paths forward.

In recent weeks Rep. Earl Blumenauer (D-OR) and Sen. Barbara Boxer (D-CA) have introduced proposals to increase revenue for the Highway Trust Fund, which Transportation Secretary Anthony Foxx warns will go insolvent by then end of the fiscal year. Neither proposal seems likely to go anywhere in this Congress, however. Look for a likely temporary reauthorization and supplementary appropriation “punt” into next year.

5 comments

[…] May Have Given Up on Infrastructure Bank, But Georgetown Public Policy Review […]

I believe that is one of the so much important information for me.

And i’m satisfied studying your article. But wanna statement on few basic

things, The site style is great, the articles is really great : D.

Excellent task, cheers

I see, that your page needs fresh and unique articles.

I know it’s hard to write posts manually everyday, but there is

solution for this. Just search in g00gle for; Atonemen’s tips

I see your blog needs some unique & fresh content. Writing manually is time consuming, but there is solution for this hard task.

Just search for – Miftolo’s tools rewriter

I see you don’t monetize your page, don’t waste your traffic, you can earn extra bucks every month because you’ve got high quality content.

If you want to know how to make extra bucks, search for: Boorfe’s

tips best adsense alternative

Comments are closed.