February 15 marked the last day of regular open enrollment under the Affordable Care Act (ACA) health insurance exchanges. The disastrous initial debuts of HealthCare.gov and other exchanges are now almost a year and a half behind us, a century in the political world. How is President Obama’s landmark heath reform doing, five years after its passage?

Political Vitality

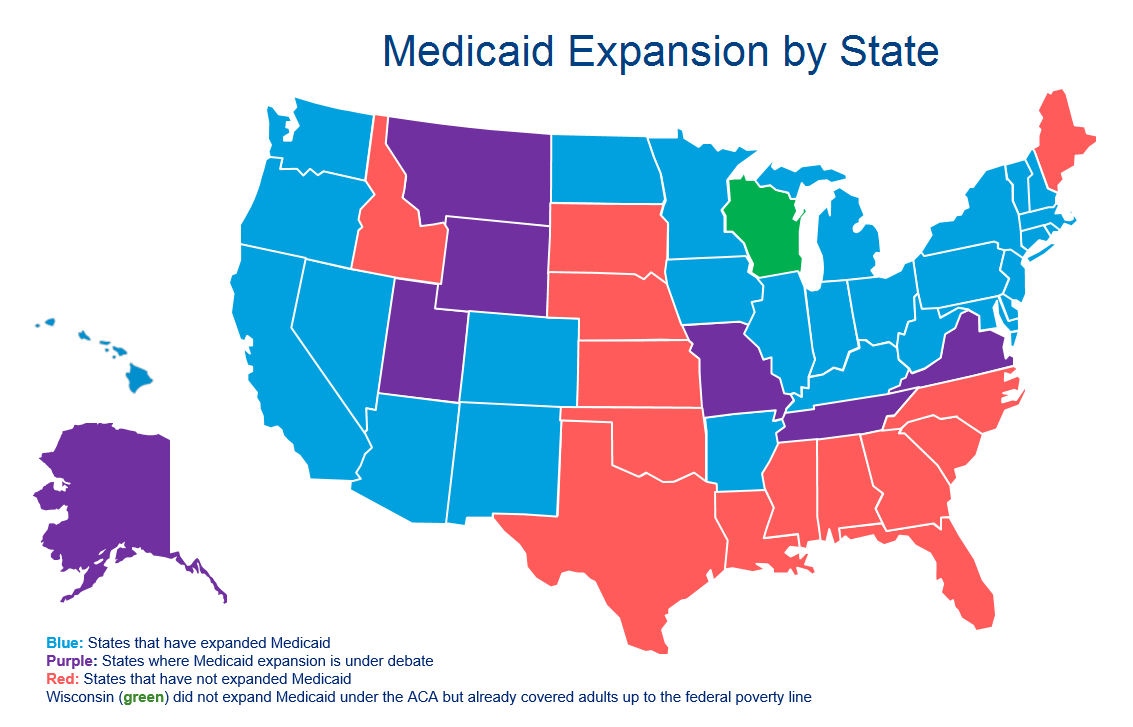

Politically, the law has survived half a decade of continuous challenges from the right, which show no sign of abating. The most significant peril the ACA has faced so far was the 2012 Supreme Court case of National Federation of Independent Businesses v. Sebelius. The Court ended up validating most of the law’s provisions, including a requirement for all Americans to have health insurance, while ruling that the expansion of the Medicaid program to all low-income adults was optional for states, a consequential decision that has resulted in a patchwork of coverage. Single adults earning less than the federal poverty guideline ($11,770 in annual income) are eligible for Medicaid coverage in 28 states and the District of Columbia, while the remaining 22 states continue to debate or rule out expanding Medicaid. The decision to expand or not fell mostly along red state-blue state lines, with some notable exceptions. Arkansas, Indiana, Kentucky, and West Virginia have expanded Medicaid, and Republican governors in Tennessee and Utah have begun championing expansion in their states.

Looking ahead, Congress and the Supreme Court will both take action that will have a huge impact on the health of the ACA this year. Earlier this month, the House of Representatives passed the first “repeal and replace” legislation of the 114th Congress, which would undo many—but not all—of the ACA’s health insurance reforms. For example, the individual mandate and the federal marketplace HealthCare.gov would be repealed, but states would be free to set up or maintain state-based exchanges. The Republican-sponsored bill would continue to prohibit lifetime limits on insurance coverage and allow for subsidies for low- to middle-income consumers to purchase insurance. With more Republican members and control of both chambers of Congress, this legislation ostensibly has a greater chance of passing, although President Obama has promised to veto any repeal attempt and the GOP lacks a filibuster-proof Senate majority (to say nothing of a majority strong enough to override a veto). In all likelihood, the latest Republican attempt at repealing the ACA will end up in the same place as the past 67 or 56 attempts (depending on whom you ask), nowhere.

The more viable threat to the ACA comes in the form of King v. Burwell, a case before the Supreme Court challenging the federal government’s authority to issue premium subsidies to consumers. The plaintiffs’ case in King argues that the text of the ACA—referring to “an exchange established by the State”—means that subsidies cannot be issued to consumers who have enrolled in HealthCare.gov and can only be issued to consumers of the thirteen states that have established their own exchanges. Following initial contradictory rulings in favor of and against the government from the Fourth Circuit and D.C. Court of Appeals, the D.C. Court reheard the case and ruled in favor of the government. The Supreme Court agreed in November to hear the case. A Supreme Court ruling for the plaintiffs would affect nearly 6.5 million consumers receiving an average of $268 per month in subsidies, rendering health insurance unaffordable for millions. However, many Republicans on Capitol Hill hope to ease the path for the Court to damage the law by minimizing disruption, potentially permitting some consumers to keep subsidies through legislative action. Even with this sort of “smooth landing,” a ruling against the government in the case would severely damage the law and embolden its opponents. The final ruling on King v. Burwell is expected in June.

Implementation Efforts

Despite the ruling on Medicaid expansion in National Federation of Independent Businesses v. Seblius, more and more states have worked on expanding the program. The majority of Americans now live in expansion states, but about four million Americans fall into the “coverage gap” of states that did not expand. Because subsidies to purchase a private plan start at an income equal to the federal poverty line, those earning less than that without demographically qualifying for old Medicaid programs (such as being disabled, blind, or eligible for Children’s Health Insurance Program) are unable to obtain insurance without purchasing it at full price, an unaffordable option for these low earners. The majority of people in this coverage gap live in the four largest non-expansion states: Texas, Florida, North Carolina, and Georgia.

However, the situation may change dramatically. Several Republican-led states have expanded Medicaid already, and more are debating the issue now. Most notable of these is Utah, where Governor Gary Herbert is in talks with the Centers for Medicare and Medicaid Services (CMS) over his Healthy Utah plan, an alternative for Medicaid expansion. Healthy Utah capitalizes on the federal money available for Medicaid expansion while adding in elements like cost-sharing for beneficiaries and a work requirement. The latter has been the main sticking points in negotiations with the federal government. Should CMS approve Governor Herbert’s plan, then that may open the door for other red states to follow Utah’s lead—new Texas Governor Greg Abbott asked his staff for a report on Healthy Utah, leading to speculation about his interest in a similar program for the Lone Star State.

That being said, the attention of most is not on Medicaid expansion but on enrollment among the federal and state exchanges. The Department of Health and Human Services already met its goal for 2015 enrollment with over 9.5 million signed up nationwide at the start of this month (and a grand total of 11.4 million as of February 15), and some of the worst fears about the individual health insurance marketplace have been unrealized: there have been no IT meltdowns on the scale of the initial debacles of HealthCare.gov or certain state marketplaces in 2013 and premiums have held steady, seen small increases, or even decreases. In fact, a rise in competition from the first year seems to have resulted in lower premiums in many areas—market forces are constraining premium inflation. This is unequivocally good news for consumers, insurance companies, and proponents of the ACA alike—so far, the health insurance marketplace has avoided fears of a “death spiral,” where disproportionately unhealthy (read: expensive for insurers) consumers enroll, causing insurance carriers to raise premiums, resulting in even more healthy people dropping out of the market, repeating itself ad nauseam.

The ACA has been the law of the land for nearly five years now and its implementation is well underway, dramatically reshaping how Americans access health care. Health reform has expanded access to insurance: only 12.9 percent of Americans are uninsured today—down from a high of 18 percent prior to the law coming into force—and insurers are unable to deny coverage based on preexisting medical conditions or to place lifetime caps on coverage. Health costs grew at their lowest rate since the Eisenhower Administration in 2013, thanks in part to the law. However, despite some measured progress in those aspects, the laws’ achievements in other areas are more mixed—the White House has pushed back deadlines for large employers to provide health benefits to their employees and has downsized goals for enrollment in the marketplaces. And the law remains as divisive politically as ever: less than half of Americans approve of the law, with a slightly larger plurality saying they disapprove, and congressional Republicans are as committed to repeal as ever. The Supreme Court may hold the future of the ACA in its hands again, as it did in 2012. If the law survives its second trial in the judicial branch, then it is difficult to imagine a scenario where it is repealed, short of a full GOP takeover of the executive and legislative branches after 2016.

Correction: an earlier version of the article characterized lower courts’ rulings in King v. Burwell as unanimous. The article has been revised to reflect the original ruling DC Court of Appeals, which found in favor of plaintiffs at first and then overturned the decision on appeal.

Feature Photos: Flickr/(Will O’Neill, Tabitha Kaylee Hawk)

Andrew Shell is Managing Editor at the Georgetown Public Policy Review and studying public policy at Georgetown University’s McCourt School. A Georgia native and 2010 graduate of the University of Georgia, he served in the Peace Corps in Ukraine for two years before moving to Washington, DC in 2013 where he currently resides.