by Alex Engler

In the past year, the United States government spent every penny that it collected. Then it went on to spend an additional $1.1 trillion, generating a deficit equivalent in value to everything produced in Mexico during that same year.

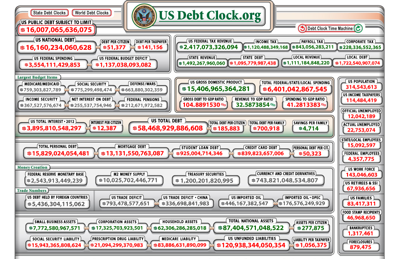

Although the fiscal 2012 deficit fell to 7.3 percent of GDP, down from 10.1 percent in 2009, this decline is the closest thing to a silver lining as anything offered in the Congressional Budget Office’s updated budget analysis. According to the CBO, the federal government now has outstanding public debts of $11.3 trillion dollars or 73 percent of the country’s $15.5 trillion GDP.

Many pundits and politicians have cautioned that there is a dangerous line at 90 percent debt-to-GDP, which the United States is rapidly approaching. They argue, based on Reinhart’s and Rogoff’s working paper Growth in a Time of Debt, that beyond this threshold national debt becomes unsustainable and dramatically constrains economic growth.

Debt-to-GDP is a favored statistic concerning the debt—many believe there is no better single number to compare a government’s financial obligation with its citizens’ potential to pay that obligation. This may be true, but this metric is still highly limited and its predictive power is diminished in the case of the United States.

Debt-to-Revenue Ratio

Among finance experts, if debt-to-GDP ratio is the golden child of budgetary analysis then the ratio of debt to federal revenue is its red-headed stepsibling.

Yet it is a substantial oversight to ignore debt in relation to government revenue. The economy at large is not directly responsible for paying down the debt – the federal government is. In light of this, contrasting debt to federal government revenue adds a beneficial context. In fiscal 2012, when the United States collected $2.4 trillion, that ratio was a stunning 464 percent.

Of course, 2012 was a year of relatively low revenue, due both to tepid economic growth and to temporary tax reductions. These factors inflate the debt-to-revenue ratio in the short term, but the fact remains that it is a staggeringly large disparity.

If the federal government was somehow capable of maintaining the current level of revenue collection and of redirecting all of it toward the debt, it would still take more than four years to pay off.

Even European nations with worse aggregate debt issues than the United States do not face such a daunting gap. Although France faces 90 percent debt-to-GDP, the revenue-to-debt ratio is just over 200 percent. Why? Where France collects 45 percent of its GDP in taxes, the United States has historically resisted an effective rate of taxation higher than 18 percent.

There is some supportive research that suggests high debt-to-revenue is a predictor of sovereign debt crises, though it is certainly not conclusive. Still, it appeals to intuition that debt-to-revenue is a proxy for willingness of a population and therefore capacity of a government to repay its debts. If so, perhaps debt-to-GDP overestimates the potential of the United States to pay down its liabilities.

The Bigger Picture

A more complete sense of the structure of United States debt requires the examination of a number of other significant obligations the country owes.

Accounting for private consumer debt, which is now at $11.4 trillion, doubles the public’s debt burden. Mortgages constitute 72 percent of this personal debt, with student loans, auto loans, and credit card payments rounding out most of what remains. Next, consider that state and local government debt piles on almost $3 trillion more. These debts (local and state government, and consumer) have been falling since 2008, but U.S. citizens are still in a deep hole.

When you combine all government debt with consumer debt, the United States collectively owes $25.7 trillion, or approximately $80,000 per citizen.

Lastly, the federal debt number used above does not include $4.8 trillion in intergovernmental holdings, which more or less equates to money collected and spent that the Treasury knows it is going to need later—most notably from the Social Security Trust Fund. Although this does not constitute debt in the sense that it is not part of the current net balance, it is important to be aware of these future shortcomings. Incorporating this liability places total federal debt closer to $16.2 trillion.

Free Debt

The United States pays the lowest interest rates of any institution on the planet. The ratio of interest payments to GDP ratio is 1.4 percent, which is spectacularly low considering how high the debt is. While that still constitutes a $220 billion fine for fiscal irresponsibility, it could be far worse.

The United States benefits markedly from being the world’s reserve currency. The United States dollar is the default for and is used in 85 percent of international transactions. Since international business requires it, foreign firms, banks, and nations must hold onto large quantities of U.S. currency. These institutions often choose to hold onto dollars in the form of Treasury notes, the most common issuance of debt. This results in higher demand for American debt and constant downward pressure on interest rates paid.

The yield on a ten-year Treasury note bought today is 1.703 percent. For investors, that is a terrible deal. In fact, adjusted for inflation, the Treasury estimates a 1.18 percent loss for an investor on the purchase of ten-year notes, while twenty-year notes are essentially a wash.

Despite these miserable returns, demand for United States debt is at an all time high. Even with its gridlocked political environment and discouraging signals from the major credit ratings agencies, investors worldwide see the United States as a safe harbor in an abnormally tumultuous market. The weak international economy, especially in the Eurozone, has drastically limited the options for low risk investment. This allows the United States to finance its debt without concern for short-term interest payments.

The Debt Outlook

The federal debt is almost certain to exceed 90 percent of GDP in the next few years, and although it is a safe assumption that this is already constraining the economy to some extent, presuming substantial economic stagnation based on this alone is myopic. There is a very strong case to begin aggressively addressing the domestic fiscal mess, but passing this particular threshold of indebtedness is simply not part of it. Too many factors unique to the United States influence both its vulnerability and resilience to debt to give credence to any theory based on one number.

Established in 1995, the Georgetown Public Policy Review is the McCourt School of Public Policy’s nonpartisan, graduate student-run publication. Our mission is to provide an outlet for innovative new thinkers and established policymakers to offer perspectives on the politics and policies that shape our nation and our world.

Humana People to People makes their task to increase under-developed

areas by way of providing coaching to primary school tutors and tradesmen,

assisting to recommend well being and give understanding of Aids and also to help

out with further developing areas agriculture.

Humana People to People assumes many different commissions

and duties all over poverty-stricken areas of nations all over the

world. Through working with the local folks and their

governing administration, capable to benefit those who are in need of assistance by their non-profit aid institutions.

China is among lots of nations this non-profit corporation goes to confront

the demanding troubles that they encounter currently.

The Humana People to People Motion works together with The

Federation for Associations from the Yunnan province of

China. The project first began within 2005 and moves on throughout today.

The Humana People to People Co-operation Work Department of the Yunnan Province functions to raise capital in order to carry

out different jobs through the entire area in poor places.

A number of developments which Humana People to People works to

take to the region of China consist of professional schools where

they could advance their education and learning, organizing them for work, presenting specifics of

transmittable illnesses and more.